Nothing Burger

Plus: This Week's Featured Place: Sitka, Alaska

Issue 61: March 28, 2022

Inside this Issue:

“Nothing” Burger: Powell Tough Talk Batters Bonds

Observe the Curve: Does Inversion Mean Recession?

Globalization Cessation? What does Fink Think?

Mobility Debility: Why Americans Don’t Move as Much Anymore

Flows or Pros? What Really Moves Stock Prices?

Ethereum Delirium: One Crypto Captain Says ETH has No Teeth

The Contractor Factor: Booz Allen and America’s Defense Spending

Greenback Attack: How the U.S. Financed the Civil War

And This Week’s Featured Place: Sitka, Alaska, Russian Roots

Quote of the Week

“Retail sales of new vehicles this month are expected to reach 1,044,500 units, a 27.8% decrease compared with March 2021 when adjusted for selling days… In April, with inventory and production levels still projected to be at historical lows compounded by global events, the overall industry sales pace will continue to be supply constrained.”

- from the latest J.D. Power, LMC U.S. Automotive Forecast

Market QuickLook

The Latest

Sometimes, just a single word can move markets. Even a simple word like “nothing.”

“Nothing,” said Fed chair Jay Powell, responding to the question: “What would prevent you from doing a 50-basis point move in May?” His cavalier dismissal of any restraints, sure enough, signaled a willingness—an eagerness, even—to do whatever it takes to slay the inflation dragon.

“Inflation is much too high,” Powell flatly stated, at a conference hosted by the National Association of Business Economics (NABE). While emphasizing that he and his FOMC colleagues haven’t made any decisions yet in advance of their next meeting in early May, he left no doubt about the ““obvious need to move expeditiously.” He’s talking of course about moving interest rates higher, following a modest quarter-point lift earlier this month.

The hawkish tone sent bond prices tumbling, as theory would predict when investors anticipate rates to rise. Some parts of the Treasury yield curve, to be sure, are rising faster than others. More specifically, shorter-duration debt is rising faster than that with longer maturities. Uncle Sam is now paying more to borrow for three years than he is to borrow for ten-years, an inversion that historically has presaged recessions. Powell dismissed this concern however, stressing the greater relevance of spreads among shorter-duration debt, which for now are still properly slowing upward (he specifically mentioned the first 18 months of the curve, rather than the often citied 2-year/10-year comparison).

Powell again made clear that he thinks the economy is in good shape (stocks reacted well to that). There are still fewer Americans working than before the pandemic. But add the number of workers plus the number of job openings, and this figure greatly exceeds pre-pandemic levels. The Fed’s best estimate is that roughly half of the decline in labor force participation comes from early retirements. In any case, Powell’s larger point is that the labor market, while booming, can’t boom for long unless price stability is re-established.

Other speakers and panels at the NABE event gave a clear window on what America’s economists are thinking about these days—Fed policy, of course, along with inflation, geopolitical unrest, labor participation, supply chain bottlenecks, oil prices and the energy transition, promoting inclusive growth, the health of the housing market, the pros and cons of a central bank digital currency, and so on. Atlanta Fed president Raphael Bostic stressed the growing trend among companies to prioritize resiliency over cost minimization, especially with respect to their international supply chains.

Regarding international business, one prominent corporate titan just declared the death of globalization. Larry Fink, head of Blackrock, wrote in a letter to shareholders: “The Russian invasion of Ukraine has put an end to the globalization we have experienced over the last three decades.” What’s more, “the large-scale reorientation of supply chains will inherently be inflationary.” Fink separately addressed the challenge of securing sufficient retirement income for all Americans—Blackrock is after all, the world’s largest money manager, championing exchange traded funds. “As people live longer and healthier lives, their risk of outliving their savings is accelerating the ‘silent crisis’ of financial insecurity in retirement.” He cited the example of a 25-year-old in 1982, who saved $10,000 in bank deposits. That would be worth approximately $50,000 today. If he or she invested in a broad-equity index such as the S&P 500, by contrast, it would be worth more than $800,000.

Retirees lucky enough to own homes, of course, are sitting pretty following an extraordinary pandemic-era spike in home values. The party is definitely slowing though, as the Fed’s pivot to hiking interest rates has its intended effect on mortgage costs. According to Freddie Mac, the average 30-year fixed-rate mortgage hit 4.42% last week. It ended 2021 at 3.11%. At one point last summer it was 2.77%. That translates to significantly higher monthly payments for borrowers, deterring demand as the latest trends suggest: The National Association of Realtors for example said existing home sales dropped 7% from January to February. Homes sales under contract but not yet finalized fell 4%.

Higher rates will impact the auto market as well. Here, the supply shortage is even more acute than in housing, owing to all those missing semiconductors. LMC Automotive and JD Power, in their latest monthly report, said U.S. retail sales of new vehicles fell a thunderous 28% y/y in March. The drop for all of Q1 should be about 15%. Americans will still spend an astonishing $125b on new vehicles this quarter, as higher prices offset the impact of fewer transactions. Automakers are earning strong profits. So are auto dealers. And here’s one more interesting piece of data from the report: Trucks and SUVs are on pace to account for a record 80.5% of new-vehicle retail sales in March. Will this change now that oil prices are spiking?

Tesla, of course, hopes more people will go electric. The company has hyper-ambitious growth plans, underscored by last week’s opening of a new plant in Germany. Germany’s Volkswagen, meanwhile, is the latest automaker to announce a multi-billion investment in North American production. In Nebraska, Warren Buffett’s Berkshire Hathaway announced a $12b acquisition—the target is an insurance company called Allegheny. The food giant General Mills expects pricing to keep pace with inflation. Uber is making peace with New York City’s taxis. Amazon faces another unionization drive.

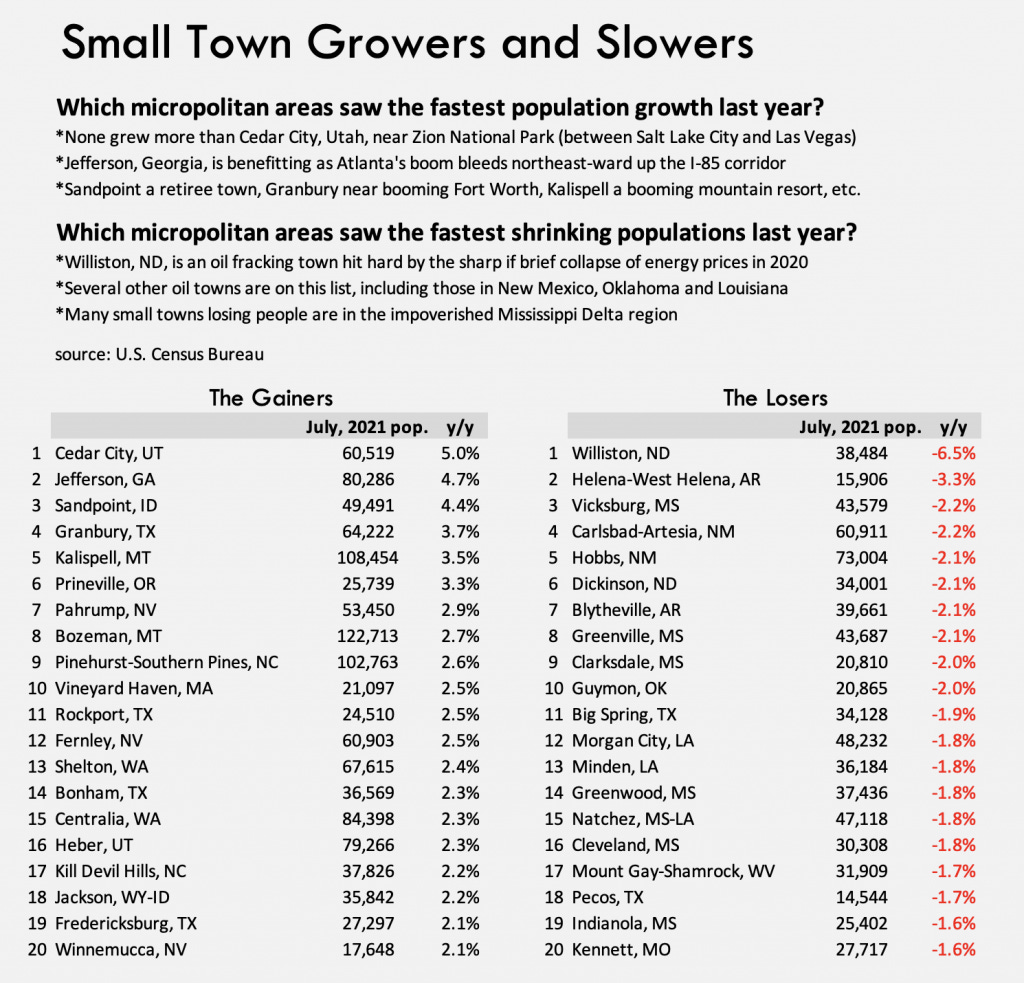

New Census data show which cities attracted the greatest population growth in the year to July 2021. St. George (Utah), Coeur D’Alene (Idaho), Myrtle Beach (South Carolina), Punta Gorda (Florida) and The Villages (Florida) top the list. No place, on the other hand, shrank more than Lake Charles (Louisiana) and Odessa (Texas), two fossil fuel centers hit hard by last year’s oil collapse but surely thriving again in 2022 as oil prices come roaring back. The next biggest population decliners were the giant cities of San Francisco, New York City and Los Angeles, with Silicon Valley (the San Jose metro) included as well. This reflects an exodus from big cities during the pandemic, along with the rise of remote work and the economic impact of absent international visitors.

Looking just at domestic migration, some surprising places saw an influx of people. Fort Myers was number one but no surprise there. Also among the leaders, however, were prominent victims of de-industrialization like Hartford, Detroit, Albany and Cleveland. All were places that were losing people before the pandemic. A renaissance in the making? Or just a momentary aberration?

With Q4, 2021 earnings season all but over, Q1 festivities are now just a few weeks away. JPMorgan Chase, whose reporting usually marks the symbolic start of a new earnings season, is scheduled to go on April 14th. But no need to wait until then for excitement. This week is a big one for government data. The Bureau of Labor Statistics will publish its jobs report for March. The Bureau of Economic Analysis, meanwhile, will publish its latest inflation index based on personal consumption expenditure (PCE). Also on this week’s agenda: an OPEC meeting that could impact the direction of oil prices. Last week, incidentally, oil prices spiked again.

Companies

Booz Allen Hamilton: Think defense contractors and which companies come to mind? As the chart below from Defense News shows, Lockheed Martin is the largest in the U.S., followed by Raytheon, Boeing, Northrup Grumman and General Dynamics. But not all defense contractors build weapons. Number 26 on this year’s Defense News list is Booz Allen Hamilton, based unsurprisingly in the Washington, D.C. suburbs near the Pentagon. It started as a general management consulting firm more than a century ago. But a contract for the Navy during World War II led to its current government focus. As CFO Lloyd Howell disclosed at an investor event earlier this month, 47% of the company’s current annual revenues come from defense consulting. Another 30% comes from civilian federal agencies, with most of the remainder from intelligence agencies. Just 2% to 3% of sales are from what the firm calls its global commercial business, often work related to cybersecurity. Booz employs about 30,000 people, many of them software engineers and data scientists. Some 70% of its workforce has a federal security clearance. An important point about the U.S. economy is that private sector contractors—including Booz Allen Hamilton—receive a large portion of the federal government’s roughly $5 trillion in annual spending. In that way, the public and private sectors are closely intertwined, especially in the defense sector but also very importantly in health care. Washington separately provides funding and credit directly to the household sector, indirectly benefitting private companies in sectors like health care, education and housing.

Tweet of the Week

Sectors

Wheat is the topic of a new “Odd Lots” podcast, featuring University of Illinois ag economist Scott Irwin. He details the current crisis now unfolding, with major supplies from Ukraine potentially unavailable. Let’s be clear about what wheat is. It’s a type of grain (other grains include corn, soy and rice) used to make food products like bread, pasta and crackers. It’s an important source of food for not just humans but animals that are raised for other food products like beef and pork. And it just so happens that both Russia and Ukraine are huge global wheat suppliers. The Russian crop will likely grow without interruption but whether it gets to global markets amid sanctions is uncertain. Spring wheat, meanwhile, needs to be planted in April or early May, which might not happen in Ukraine this year due to the war. Winter wheat, to be clear, which is planted in the northern hemisphere’s autumn, is produced in much larger volumes than the spring crop. But the world market could be extremely short this summer, to a catastrophic degree in import-dependent countries like Egypt. Irwin stresses the inter-connectedness of commodities—pigs eat wheat products, for example, so higher wheat prices will mean higher pork prices. There’s also the issue of fertilizer, whose supplies from Russia and Belarus are threatened, leading to a big price spike for farmers. In any case, commodity traders will play a key role in getting sufficient supplies of food to where they’re needed. The four big ones are the so-called ABCDs: Archer-Daniels-Midland, Bunge, Cargill and Dreyfuss (with Glencore’s Viterra unit trying to play in the space as well). Separately, Javier Blas, who co-authored a book about the ABCDs (see Econ Weekly from March 8, 2021), wrote last week about one grain product that’s thankfully not in short supply right now: Rice, a critical food staple for much of Asia.

Housing: Americans are moving less. During the 1980s, according to the Census, nearly a fifth of all Americans in any given year were moving to a new home, either within the same state or in a different state—the figures include people moving to the U.S. from abroad as well. That’s consistent with the narrative of America being a very mobile society since its origins—people constantly moving within and foreigners constantly arriving. Mobility, however, has been steadily declining since the 1980s, with just 10% of people moving in 2019. Rates have dropped even more during the pandemic. Why? The culprit seems to be a lack of affordable housing in places with lots of open jobs. In the 19th century, Americans moved ever farther west seeking employment. Throughout the industrial era, Americans—including African Americans from the South—moved into northern factory cities like Detroit. De-industrialization led people away from the north and into rising Sun Belt cities like Las Vegas and Atlanta. The Sun Belt lurch continues, albeit more slowly as the mobility data show. The jobs are there but the housing isn’t. That’s actually more true of superstar cities (see the Places section below) like San Francisco and New York, where it’s challenging to live without a household income that’s way above the national average. That eliminates most civil servants like teachers and firefighters, or workers in retail, hospitality and transportation/logistics. It’s a reminder that America (and many other developed economies for that matter) have a housing shortage problem, one that’s great for incumbent homeowners enjoying rising prices but bad for mobility—and by extension the economy.

Markets

Stocks: Tracy Alloway of Bloomberg’s aforementioned “Odd Lots” podcast likes to call it “flows before pros.” It’s the idea that stock prices are determined more by the flows of money into and out of the market, rather than fundamental valuations as calculated by professional traders. Hari Krishnan and Ash Bennington, in fact, wrote a book about the idea, called “Market Tremors: Quantifying Structural Risks in Modern Financial Markets.” According to classical valuations of stocks, they explained on the “Hidden Forces” podcast, prices should adjust to exogenous factors like an earnings release, new financial guidance or geopolitical events. In other words: “Everything is priced fairly until news comes in, and prices adjust.” In reality, they argue, price movements are greatly influenced by the flow of dollars—who has them to sell, who has them to buy, how many of them is the Fed creating, and so on. Also influential is the derivative market, where lots of money flows into and out of stocks according to the behavior of risk managers and speculators. This was clearly the case when options trading caused meme stocks like GameStop and AMC to skyrocket in early 2021. Krishnan and Bennington talk about other forces shaping modern financial markets, including the rise of passive ETF investing, bank regulations and the practice of investors crowding into specific asset classes or strategies.

Abroad:

Toronto: It’s not quite Silicon Valley, or even New York City. But Toronto, according to a New York Times profile, is now the third largest tech hub in North America. The real estate firm CBRE, in fact, ranks it much larger by number of tech workers than up-and-coming U.S. technology hubs like Austin and Miami. Two big reasons are the University of Toronto and the nearby University of Waterloo, serving a similar incubator role as Stamford University in Silicon Valley. Also critical: Canada’s relaxed immigration policies, luring global talent no longer welcome south of the border—U.S. immigration rules have tightened significantly in recent years. Toronto’s average tech worker salaries, meanwhile, are lower than they are in Silicon Valley. Toronto happens to be the fourth largest city in North America by population (nearly half of its residents are foreign born); only Mexico City, New York City and Los Angeles are larger. Shopify, an e-commerce platform challenging Amazon, is a home-grown corporate resident. But U.S. superstar firms like Google and Facebook have large Toronto offices as well. The University of Toronto is currently building a complex to house artificial intelligence and biotech companies. The government of Ontario, furthermore, recently outlawed enforcement of noncompete contract clauses, which can be an impediment to would-be entrepreneurs. Keep in mind though: “Investment in new Toronto companies is still tiny compared with Silicon Valley,” the Times writes. “In 2021 and 2022, investors pumped $132b into Silicon Valley tech start-ups, according to the research firm Tracxn. In Toronto, that figure was $5.4b.”

Government

State and Local Government (SLG): The National Association of Homebuilders, in its “Eye on Housing” blog, gives a breakdown of where the SLG sector generates its tax revenue. Nationwide, 36% comes from property taxes (mostly on residential or commercial land and buildings, and mostly levied by counties, cities, municipalities, school districts, water authorities, etc.). Another 31% is from income taxes on individuals. Sales taxes are responsible for 27%. Much of the remaining 6% is from income taxes on corporations. These figures, of course, vary by state and locality, with some depending more on this or that tax. According to the Urban Institute, New Hampshire and New Jersey are most dependent on property taxes. Alabama, Arkansas and Delaware are at the other end of the scale. Nevada and Washington are most dependent on sales taxes, while five states don’t even have a sales tax (Alaska, Delaware, Montana, New Hampshire and Oregon). Alaska, thanks to its oil wealth, doesn’t levy income taxes either. Same for Florida, Nevada, South Dakota, Tennessee, Texas, New Hampshire, Washington and Wyoming. Are taxes the only source of revenue for the SLG sector? No, it also receives direct transfers from the federal government—Montana depends most on federal transfers, Hawaii the least. States also charge fees for various services, including tuition for public colleges, payments at public hospitals and roadway tolls. South Carolina depends most on these fees, Connecticut the least.

Places:

Sitka, Alaska: Long before tensions over Ukraine, long before the Cold War and long before even their alliance in World War II, the United States and Russia made a deal. It was 1867, a few years after the American Civil War, and a year after Russia’s defeat in the Crimea War. The Russian Czar had war debts to pay. So he gladly accepted $7m in gold from the Americans, in exchange for the barren lands of Alaska, where Russians had established small settlements and fur-trading businesses. A grand “folly,” some in the U.S. Congress said at the time. Even so, the deal was approved, and the transaction sealed on October 18, 1867. A ceremony was held in Russia’s Alaskan capital: Sitka. Today, a Russian Orthodox church still stands in Sitka’s city center, a rebuilt version of one originally constructed in the days of Russian rule. It’s one of many reasons why 200,000 tourists were expected to visit in the summer of 2020—that is, before Covid mothballed the cruise industry. Most come for the stunning natural beauty and exotic wildlife. And come they will: Officials expect a record-breaking tourist season this summer. A year ago, Econ Weekly profiled the economy of nearby Juneau, also located amid the archipelago of islands stretching down the coast of southeastern Alaska. A key theme was seafood, likewise a staple of the Sitka economy. The city is home to three large processing plants including Silver Bay Seafoods, the largest. It’s also the base of hundreds of commercial vessels, most operated by self-employed commercial fishermen. The economics of the seafood industry aren’t easy, not with competition from lower-wage countries like China, and Russia too before recent events. Labor at home is hard to come by, so the processing plants have long recruited from as far away as Asia, Latin America and Eastern Europe. They’re in fact among the most prolific issuers of foreign H2-B visas authorized for temporary non-agricultural jobs. In 2019, non-Alaska residents (including seasonal workers from Seattle and elsewhere on the U.S. mainland) accounted for 34% of Sitka’s workforce. According to the Sitka Economic Development Association, the city ranks as the 15th busiest seafood port in the U.S. based on value (major products include salmon, halibut and black cod). Sitka’s single largest employer is the local hospital. Though the state capital moved to Juneau a few decades after the Russians left, government work is still a major component of Sitka’s labor market. The U.S. Coast Guard and the U.S. Forest Service have sizeable footprints. Another notable employer is the Sitka Tribe of Alaska (STA), a federally recognized government entity representing Native peoples including the Tlingit tribe. The Tlingit have inhabited the area for thousands of years, at one point engaging in military conflict with Russia. The Census counts about 12% of Sitka’s population as Native American. Roughly 8% are Asian and 7% Hispanic. Overall, the population of about 8,5000 is shrinking and aging, a big reason for the seafood sector’s labor shortage. One thing that’s definitely not in short supply though, is fresh water and cheap hydropower. Is Sitka wealthy? It does have a rather high median household income of $82,000, compared to $78k for all of Alaska and $65k nationwide. Alaskan residents should get a big check next year thanks to high oil prices—the state redistributes much of its oil wealth to Alaskans through an annual dividend payment. Imagine, by the way, if Russia had kept Alaska. It would be an even larger oil power today, never mind all the gold that was discovered a few years after the sale. Understatement of the century: That $7m sale turned out to be a pretty good deal for America. (Source: Sitka Economic Development Association, Sitka Salmon Shares, U.S. Census, Southwest Alaska Municipal Conference, Northern Southeast Regional Aquaculture Association).

Sitka: One more thing about Sitka’s history when it was still part of Russia. This is from the Sitka Economic Development Association: “During the mid-1800s, Sitka, known as the ‘Paris of the Pacific,’ was the largest, most industrious city on the Pacific Rim, with Canton, China and San Francisco, California following behind. Ships from many nations visited the port. Furs, salmon, lumber and ice were exported to Hawaii, Mexico and California. There was an active shipyard and foundry.”

Atlanta, Dallas, Denver, San Diego, Salt Lake City, Orlando, Kansas City, St. Louis: These are some of what the Brookings Institution calls “rising star” cities—places attracting lots of new people, capital, companies and workers. They’re benefiting from the boom in remote working, a pandemic-era phenomenon that’s simultaneously erasing jobs from superstar metros like Boston, the San Francisco Bay Area, New York and Los Angeles. Between 2010 and 2019, Brookings notes, the U.S. tech sector grew by 47% and added more than 1.2m jobs, nearly triple the growth of the economy as a whole. But a lot of this growth was concentrated in the superstar coastal cities—just eight of them (San Francisco, San Jose, Austin, Boston, Seattle, Los Angeles, New York and Washington, DC) accounted for nearly half of all tech job creation in the latter half of the decade. More recently, however, Silicon Valley companies like Palantir, Hewlett Packard Enterprise, Oracle and Tesla have moved inland to places like Colorado and Texas. Intel announced a giant new investment near Columbus. And so on, hinting at a possible decentralization of the nation’s tech sector. Tech growth in superstar cities is now slowing, while taking off in not just the rising cities listed above but also northern business centers (Philadelphia, Minneapolis, Cincinnati); warm-weather cities (Charlotte, San Antonio, Nashville, Birmingham, New Orleans, Greensboro, Jackson, Stockton); university towns (Chapel Hill, Madison, Boulder, Lincoln, Tallahassee, Charlottesville, Ithaca); and Sun Belt vacation and retiree spots (Virginia Beach, Ogden, Albuquerque, Tucson, El Paso, Santa Barbara, Barnstable, Gulfport-Biloxi, Pensacola, Salisbury). The Brookings report emphasized that “the tech industry still remains more a “winner-take-most” affair,” with most jobs still concentrated in those superstar cities. But “intriguing signals point to possible decentralization.”

Looking Back

The Civil War: The government had no authority to raise taxes, no national bank, no national currency. This was the situation on the eve of the Civil War, as Roger Lowenstein describes in his new book “Ways and Means: Lincoln and His Cabinet and the Financing of the Civil War.” In fact, the federal government at the time was really just the Post Office and a modest-sized army, funded mostly by tariffs on imports and taxes on products like whiskey. So how was Washington supposed to pay for the conflict? The job went to Lincoln’s Secretary of the Treasury Salmon Chase who was able to borrow some money from banks but not nearly enough. With the support of Congress, which at the time held more economic power than the presidency, Chase managed to implement the nation’s first progressive income tax. He also created a national fiat currency (not backed by gold or silver) dubbed the “Greenback”—until then individual banks across the country issued their own currencies. Printing the new greenbacks led to inflation as high as 80% over the course of the war. But that was nothing compared to the 9,000% inflation experienced within the Confederacy. The South, for political and philosophical reasons, couldn’t tax incomes. And almost all the region’s wealth was tied up in slaves and land, producing cotton that couldn’t get to Britain’s textile mills because of the Union blockade.

The Civil War: Lowenstein makes the broader point about the Civil War being revolutionary for federal government expansion (as wars and national emergencies often are). In addition to the new income tax and national currency, Congress in the early 1860s created the Homestead Act granting western land to settlers, established land grant colleges and created the Department of Agriculture, supporting what was then the country’s largest industry. After the Civil War, the income tax disappeared, returning in modest form in 1913, and then with large revenue-raising power a few years later to finance World War I. The U.S. kept its greenbacks after the Civil War but anchored their value to gold prices. Things stayed that way even after the Federal Reserve opened in 1913. Not until the Great Depression in 1933 did Washington end the gold standard domestically. The dollar remained convertible to gold for international transactions however, until that is, President Nixon ended all gold convertibility in 1971.

Looking Ahead

Crypto Economy: Sam Bankman-Fried is the billionaire founder of FTX, one of several crypto exchanges that advertised in this year’s Super Bowl. Naturally, he’s bullish on the emerging crypto economy, a virtual world where information and data can be verified without verifiers (a decentralized network of computer “miners” takes care of that). Bankman-Fried, however, in an interview with George Mason’s Tyler Cowen, expressed bearishness about Ethereum, the world’s second most owned crypto-asset after Bitcoin. Ethereum is designed to be a platform for automated “smart” contracts between two parties. But its ability to process transactions is far too slow to gain traction—just 10-to-15 per second, compared to the millions that payment platforms like Visa and MasterCard can perform. Bankman-Fried thinks the Ethereum blockchain might be able to reach a few thousand per second but that still won’t be nearly enough to handle demand. A technique called sharding will help—that’s when multiple blockchains run in parallel and then synch up with each other. But he says blockchains don’t talk to each other easily, and in any case, this would complicate transactions.