GDP Contraction as Fed Prepares for Action

Plus: This Week's Featured Place: Susanville, CA, Prisoner’s Dilemma

Inside This Issue:

GDP Surprise: Oh My, a Shrinking Pie

The Latest on Prices: Inflation Loses Heat as Fed Prepares to Meet

Big Tech Big Five: Supremely Profitable but Not Invincible

The Great Reversal: In a Shift, Asset Prices Falling, Consumer Prices Gaining

Lith Making: Tesla and Other EV Makers Need More Lithium

Bear Market: A Look Back at the Fall of Wall Street Titan Bear Stearns

Biotech in Boston: Kendall Square, a Life Science Lair

What If There’s Another Crisis? What Happens Then? Could the Fed Stim Again?

And This Week’s Featured Place: Susanville, CA, Prisoner’s Dilemma

Reminder: The Econ Weekly podcast is now available on iTunes, Stitcher, Google Podcasts and Spotify. Just search for Econ Weekly and please leave a review to help spread the word.

Quote of the Week

“We have to watch that balance between the strength of the consumer, as well as what we see in the input costs, etc.… But right now, we see nothing but strength in the consumer and the demand for GM products.”

-General Motors CFO Paul Jacobson

Market QuickLook

The Latest

Did the U.S. economy really shrink in the first quarter of 2022? That’s what the Commerce Department’s latest GDP figures say. From January to March, domestic production, adjusted for inflation, declined 0.4% from the previous quarter, or 1.4% when multiplied by four (to get the annualized figure). It’s a far cry from the vigorous 6.9% y/y growth recorded just one quarter earlier. Is a recession already underway?

Take a deep breath. The ugly Q1 figure, just like the flattering Q4 figure, was heavily influenced by the rate of change in inventories held by businesses, which the Bureau of Economic Analysis (the folks who do the calculations) calls “one of the most volatile components of GDP.” What’s more, recent inventory swings have a lot to do with what’s happening in the semicon-deprived auto sector—it’s a big sector for sure, but not especially representative. Separately, the Q1 GDP drop was also tied to a drop in government spending, notably defense spending which is poised to soon grow again.

More importantly and relevantly for the economy, the Q1 GDP figures showed that businesses are still investing. And most importantly and most relevantly, households are still spending. Spending in fact grew nearly 3% y/y, despite the omicron setback early in the quarter. Some of that spending, to be sure, was on services and especially goods produced outside of the U.S., which later gets removed from the GDP calculation when subtracting net exports. But this doesn’t negate the point: Americans—thanks largely to a bustling job market and savings amassed during the pandemic—are still spending. Companies, one after the other, are indeed making that crystal clear in their Q1 earnings calls (see the GM quote above). Companies are still earning robust profits as well, which pours more cold water on the thesis that the U.S. economy is already in recession. It’s surely not.

Reassuring news for the Fed, no, as it prepares for its big meeting this week? At the same time, there’s more evidence that prices are cooling off a bit. According to the PCE price index for March, inflation was up 6.6%, or just 5.2% excluding food and energy (which are notoriously volatile). The month-to-month rate ex food and energy was just 0.3%.

Wow, nothing but positive news. Um, maybe not. Yes, it’s true, the American consumer is strong. Corporate America is strong. And inflation is showing a few signs of moderating. That’s quite a fortress. But against this fortress, gale-force winds are blowing.

Inflation, of course, is one of those headwinds. It remains a major headache for households and businesses. Same for supply chain disruptions, which are driving much of the inflation. In some respects, supply-side pressures are easing, with GM and Ford for example both seeing somewhat better availability of semiconductors. On the other hand, supply-side problems could get worse, not better, because of factory and port closures in China (Ford, for one, has 50 major suppliers in the Shanghai-area alone). The Ukraine war presents additional risks. And back home, labor supply remains extremely tight.

That said, American workers are earning less after adjusting for inflation. Real wages during Q1 fell nearly 4% y/y, with government workers seeing an even bigger dip. Workers are getting raises, yes. But these are not keeping up with price inflation. Looking at disposable income (which includes other income besides wages), the declines are even sharper. Americans, alas, are supporting their robust spending by dipping into their savings (which make no mistake, grew a lot thanks to aggressive fiscal stimulus measures during the pandemic).

Oil prices topping $100 a barrel is a further drag, making it pricier to move goods and gas-up the family car. A weakening global economy doesn’t help. The critical housing market is unambiguously cooling, with home sales declining 9% from February to March, and 13% from last March. It’s no bubble, to be clear. And for that matter, even the last bubble wasn’t really a bubble— average home prices are now 69% above their 2007 peak. Still, the slowdown is palpable.

Some spot a trucking slowdown too, though that’s subject to debate. The stock market is unmistakably retreating—the tech-heavy Nasdaq is down by more than a fifth since the start of this year. The bond market certainly isn’t thriving, with rising interest rates hitting hard. A strong dollar puts pressure on U.S. exporters. Like homebuyers, companies (especially those with weaker credits) face more expensive financing. Fading fast now are the carnival market memories of 2021: meme stocks, SPACs, crypto-coins, your grandma’s new tech startup… everything was coming up roses. A young electric vehicle maker like Rivian? Buy, buy, buy!

It’s now bye, bye, bye to those days. In Rivian’s case, a freefalling stock wiped red ink all over the income statements of two of its prominent shareholders, namely Amazon and Ford. Even more symbolic of the pandemic-era hype? The online trading platform Robinhood, which saw Q1 revenues tumble 43% y/y. It also lost nearly $400m and will shrink its workforce by almost a tenth.

It’s almost as if the world of the past 40 years is reversing: instead of asset prices perpetually gaining and consumer prices perpetually stable, it’s been the other way around in 2022. We’ll see if there’s any resiliency to this new trend, which there might be if housing prices begin showing declines. In the meantime, other shorter-term trends tied to the pandemic are clearly reversing: Americans are now spending more on services rather than goods, for example, and spending more at physical stores rather than online.

The latter switch puts some pressure on Big Tech’s Big Five, notably Amazon, Alphabet and Facebook (see the Companies section below). Everyone, of course, would rather talk about Elon Musk and his Twitter escapades. But in Detroit, Ford and GM were focused on their electric vehicle ambitions, and beyond that their vision for autonomous vehicles. Ford last week debuted its newest F-150 pickup, an electric version of America’s best-selling vehicle. The new Lightning F-150 is in high demand but supplies are limited (a metaphor for the economy, no?). As Autoline Daily pointed out, it uses about 1,700 microchips, compared to more like 200 for the ICE version.

ICE vehicles, make no mistake, aren’t disappearing anytime soon, which is good news for oil companies, this year’s best stock market performers. Berkshire Hathaway, which held its always lively annual meeting on Saturday, knows that well from its holding of Occidental Petroleum. Chevron, in its Q1 earnings call, says oil prices could see further upward pressure because international air travel hasn’t yet recovered, China is still in lockdown, independent shale producers are prioritizing cash returns to shareholders (over drilling) and global energy giants are shifting investments to green energy. “Recent events remind us,” Chevron said, “of the importance of energy.”

No reminders needed of this week’s big event. Get ready. The Fed will make is big interest rate announcement on Wednesday.

Companies

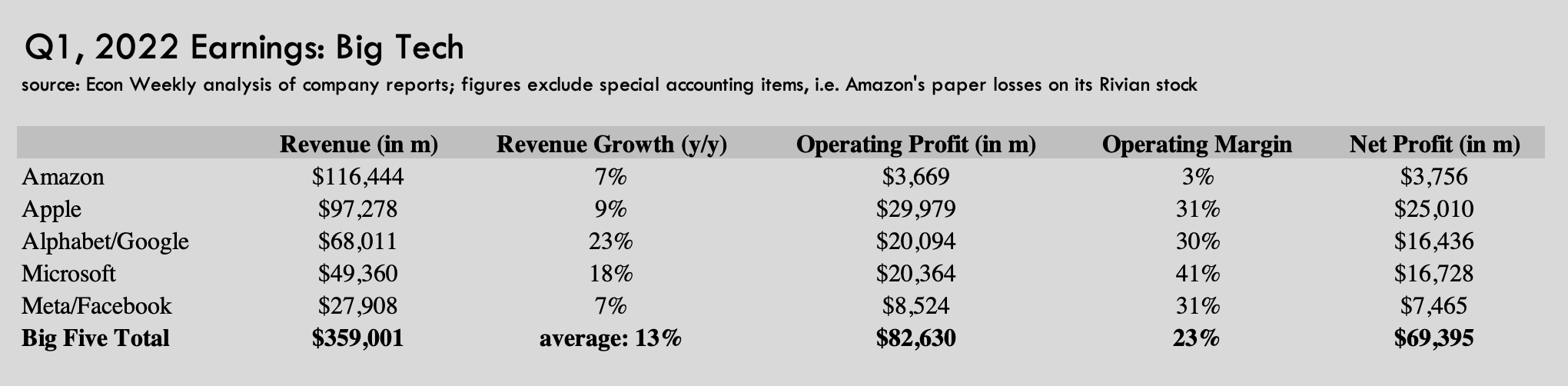

· Apple, Amazon, Microsoft, Alphabet and Meta: As usual, the “Big Tech Big Five” reported astoundingly enormous revenues, collectively reaching $359b for just the three months that ended in March. That’s roughly 90 days of revenue equivalent to the entire GDP of Egypt. Their collective Q1 operating profits, meanwhile, reached $83b, further underscoring the importance of Silicon Valley and Silicon Seattle to the modern American economy. The Big Five overlap and compete in some critical markets—Meta vs. Alphabet in online ads, for example, or Amazon vs. Microsoft vs. Google in the Cloud. But they each have distinct business models. All are both revered and often controversial. All are among the country’s largest spenders on research and development. All are at the cutting edge of information technology, including machine learning. Their financial muscle and political clout, meanwhile, approximates that which railroads, Wall Steet and oil companies wielded in decades past. At the same time, the Big Five face some important vulnerabilities, some of which are highlighted in the chart below.

· One specific vulnerability is the subject of Tim Hwang’s book “Subprime Attention Crisis: Advertising and the Time Bomb at the Heart of the Internet.” Online advertising, he writes, generates 90% of Meta’s revenue and 80% of Alphabet’s revenue. They earn it by connecting advertisers with targeted customers, which they can do effectively because of everything they know about all the billions of people that use their services (i.e., search for info on Google.com or post photos on the Instagram app). It’s a form of advertising, the companies boast, that’s more measurable and trackable than say, T.V. or radio advertising. Hwang, though, questions its effectiveness. He points to Google’s own research that suggested that half of online ads are never even seen. There’s the threat of ad blocking software. Recommendation algorithms, furthermore, are often not very good—he cites the case of someone that ordered metal address numbers for his mailbox on Amazon, which prompted the latter’s algorithms to start suggesting other numbers he might like. Hwang said Procter & Gamble, one of the world’s largest advertisers, recently cut $200m from its online ad budget without much effect. A business—data-driven, micro-targeted ads—that “might be based on nothing?” An unconventional view for sure, but an interesting one. In a related point, The Economist notes that online ad spending is heavily concentrated among a few big spenders, typically retailers, financial services firms and travel companies (think Home Depot, Geico and Expedia).

Tweet of the Week

Sectors

· Private Prisons: In 2014, The Atlantic magazine ran a story about rural America’s “prison industrial complex.” Panicked amid disappearing coal mines, shuttered factories and other severe setbacks, many small towns began building prisons as an economic development tool. The prison population, after all, was growing sharply due to tougher sentencing laws. Prisoners themselves, besides, are a source of low-wage labor. But more important, as the article describes, is the “industry that springs up around the prison system.” It continues: “First, someone will be contracted to build the prison. Then you’ll need a staff for maintenance. Next comes the restaurants and hotels in the nearby town that feed and house relatives coming to visit the incarcerated in these far-off places. When you’re finished, you have an entire local economy dependent on the existence of a prison.” Susanville, California (see below), is one such rural area. Franklin Township in far upstate New York (profiled in the Oct. 9th issue of Econ Weekly) is another. Alabama, a mostly rural state, is now using federal stimulus funds to build two new prisons. In Florida, the state legislature is considering construction of two new 4,500-bed correctional facilities as part of its modernization program. In 2020, according to the U.S. Justice Department, 1.4m Americans were held in federal and state prisons (this doesn’t include another 750,000 or so in local jails). But this 1.4m was down by a quarter from 2010. Simply put, Americans aren’t locking up as many people anymore, following a dramatic increase in the 1980s and 1990s. Indeed, in 2020, the imprisonment rate was 459 per 100,000 American adults, the lowest since 1992. Most of America’s prisons are government-run operations. But some are outsourced to private-sector companies, including GEO Group and Core Civic, both publicly traded. In their latest earnings calls, they discussed how they’re dealing with declining inmate populations—in GEO’s case, seven of its Justice Department contracts were not renewed last year. These firms also have contracts with the Department of Homeland Security’s U.S. Immigration and Customs Enforcement (ICE), which should see a surge in demand for detention capacity once Title 42 is rescinded (that’s a Covid-era authority that allows immigration officials to expel illegal border crossers without access to asylum hearings). Private prison firms also provide services like electronic monitoring of non-incarcerated offenders—in 2020, roughly 4m Americans were not behind bars but still under the supervision of adult correctional systems. During the Covid crisis, many prisoners were given furloughs, home confinement or early releases to enable more social distancing within facilities. Do these companies make money? In 2021, Core Civic reported a $127m net profit adjusted for special items on $1.9b in revenue. Geo Group, which by the way runs America’s largest private prison in Baldwin, Michigan, earned a $159m adjusted net profit last year, on $2.3b in revenue. A few final points about the U.S. federal and state prison population: Nearly half of all inmates are serving sentences for drug offenses. Just 8% are in for violent crime. Most of the rest are guilty of what’s called “public order” offenses, ranging from illegal weapons possession to tax violation. For the most dangerous and notorious inmates, like the drug lord El Chapo and the Boston Marathon Bomber, the U.S. has what’s called a “Super Max” prison in rural Colorado. The military runs detention facilities as well, most famously in Guantanamo, Cuba.

Markets

· Lithium: During Tesla’s Q1 earnings call, Elon Musk mentioned lithium as one of the “limiting factors for accelerating the advent of a sustainable energy future.” In fact, the word lithium was mentioned 26 times during the call, underscoring its importance to electric vehicle batteries. Musk emphasized that there’s absolutely no shortage of lithium on earth. But it needs to be extracted and refined, a process requiring lots of industrial equipment. And there’s simply not enough of this happening, despite soaring prices that you’d think would make it an attractive investment. Indeed, lithium happens to be the single biggest cost growth item for Tesla in percentage terms.

· Savings: Synchrony Financial, a Connecticut company once part of GE, said one-third of U.S. consumers have depleted the entirety of the cash stimulus the received from Uncle Sam during the past two years. But the other two-thirds still have either all or part of it still saved.

Government

· Monetary Policy: Economists celebrate former Fed chief Paul Volcker as the person who slayed the inflation dragon of the 1970s by sharply raising interest rates. Eric Leeper, though, adds the point that fiscal policy also played a role. Leeper, a University of Virginia professor and former Fed economist, explained on the Macro Musings podcast that Congress—after a big tax cut in 1981—raised taxes four times during the 1980s. For inflation fighting to work, he concludes, “tight monetary policy has to be followed by tight fiscal policy.” This raises the question: How about now? Will Congress raise taxes to complement the Fed’s rates hikes? If the FOMC winds up moving overnight interest rates to 5%, as economist Larry Summers for one has suggested, this would balloon the Federal debt by $1 trillion. That’s a lot more money, i.e., Treasury securities, that the Fed would need to “print.” Higher taxes might be the only way to offset the inflationary effects of that.

· A quick reminder on specifically how the Fed alters overnight interest rates, and how its method changed during the 2008-09 financial crisis. Pre-crisis, the Fed could move overnight rates where it wanted by adjusting the amount of bank reserves in its system (banks hold reserves with the Fed to satisfy regulatory requirements and ensure they have enough liquidity to meet day-to-day needs like ensuring uninterrupted flows of interbank payments). That was then. During the 08-09 crisis, the Fed created so many new reserves that the old way of doing things no longer worked. So the Fed has since manipulated rates by paying banks a chosen interest rate on those reserves, and by offering nonbanks (that don’t have accounts with the Fed) an alternative way of earning a small return in the overnight “repo” market. The two rates together provide a ceiling and a floor for overnight rates, or what the Fed calls its target range. The current floor is 0.25%. The current ceiling is 0.50%. But expect that range to increase by at least a quarter point at this week’s big meeting.

Places:

· Susanville, California: The history will sound familiar. Like so many towns in the American West, people originally came for the mining, the farming and the logging. Today, however, the people of Susanville, a town in remote northeastern California, depend for their livelihoods on something altogether different, a local industry, in fact, facing a major crisis. This is not the California you see on T.V. No Hollywood movie stars. No billion-dollar tech startups. No cutting-edge aerospace companies, tourist-filled beaches or world-class farmland. The economy in Susanville revolves around just one thing: Prisons. Three of them in fact, two run by the state of California and one by the Federal government. One of the state facilities, however—the California Correctional Center (CCC)—is slated for closure in June. It’s part of the state’s plan to cut $172m from its $14b prison budget. And it reflects a national trend to reverse a decades-long surge in the number of incarcerated Americans. Susanville’s economy, as a result, faces ruin. The three prisons provide roughly half of the town’s employment. And much of the other half—local government, retail, health care, etc.—depends on the incomes of prison workers. Even the local community college gets by with significant enrollment from Susanville’s prisoners. A documentary about the town produced by No Way Back profiled a small business owner with a contract to provide milk and other dairy products to the prisons. With all of this now threatened by the CCC closure, Susanville’s real estate values are plummeting. Residents with the means are leaving, accelerating a long-run population drop reflective of declines throughout rural America—Susanville saw its non-prisoner population shrink 14% in the 2010s. The prison population, meanwhile, is about 6,000. There’s a small Indian Reservation in the middle of town, where the tribal government runs a modest casino and hotel. There’s a Walmart in town too. But the best-paid jobs are those in the prisons, specifically prison guards represented by one of California’s most powerful unions, the California Correctional Peace Officers Association. With two large prisons remaining after CCC’s closure, Susanville will still have plenty of state and federal money flowing in. But it seems inevitable that the economy will shrink sharply from its current level. A once-vibrant sawmill industry is long gone, with the last mill closing in 2004. The town’s efforts to reinvent itself are challenged by the area’s remoteness, and the fact that just 6% of residents over 25 have college degrees. Reno, a booming economy across the border in Nevada, is 1.5 hours away by car, making it a difficult daily commute. Sacramento, California’s capital, is 3.5 hours away. Still another threat to Susanville: Destructive fires and droughts. As for basic local services like police and fire protection, the town has some breathing room thanks to the American Rescue Plan Act that Congress passed last year. ARPA, officials say, “provides the city with some time to research revenue increasing or cost saving items that may preserve the city’s ability to provide the vital services at the level our citizens are accustomed.” But it adds “the City’s General Fund financial situation is serious, and the city cannot continue to operate at its current service levels unless revenues increase.” (Sources: U.S. Census, San Francisco Chronicle, Los Angeles Times, U.S. Bureau of Prisons, Congressional Research Service).

· Boston: Kendall Square isn’t nearly as well-known as Silicon Valley. Come to think of it, it might not even have the same level of recognition as Route 128, the Boston area’s Silicon Valley-like tech corridor. Kendall Square though, in the Cambridge neighborhood in the heart of Boston, has become what Robert Buderi calls the “biotech capital of the world.” Buderi’s new book is called “Where Futures Converge: Kendall Square and the Making of a Global Innovation Hub.” It’s a history of the area, which lies within walking distance of both Harvard and MIT Universities, two of the world’s most prestigious. Today, the neighborhood’s most famous company is Moderna, whose mRNA helped greatly in the struggle against Covid-19. The square is also home to Biogen, the area’s first major biotech firm. Another big player is Genzyme. According to the Boston Herald, there are more than a hundred biotech firms in just one square mile. “Kendall Square is simply the densest collection of life scientists in the known universe,” said Eric Lander, director of the Broad Institute of MIT and Harvard, speaking with the Herald in 2020. Research labs are everywhere, as are the many professionals catering to these scientists—real estate agents, lawyers, doctors, etc. But Kendall Square wasn’t always about biotech. Long ago, it was a center for developing rubber products and railroad cars. It was home to the camera company Polaroid and Lotus123, which made spreadsheet software before the days of Microsoft Excel. Today, Big Tech firms like Amazon and Google have a large footprint in Kendall Square as well.

Looking Back

· Bear Stearns: Jeff Snider, whose Eurodollar commentary has become somewhat of an internet sensation among financial wonks, gave a good synopsis of what happened to the investment bank Bear Stearns in the run-up to the 2008 financial meltdown. During the early 2000s, he said, financial markets depended on the practice of taking illiquid loans like subprime mortgages and turning them into “safe” assets through various fancy forms of securitization. One purpose was to use these assets as collateral to borrow, often in the overnight money market. That’s how firms like Bear Stearns operated—they ensured they had enough cash on hand each day through overnight borrowing, in those days from other banks like JPMorgan. When it became clear that these assets weren’t so safe, however, JPMorgan told Bear Stearns it would need a lot more collateral if it wanted to keep borrowing. Increasingly, overnight lending counterparties stopped accepting junk mortgage securities as collateral, demanding super-safe Treasuries instead. Bear Stearns eventually lost access to the overnight lending market and collapsed, ultimately swallowed by JPMorgan itself. One final point to remember: Bear Stearns was an investment bank, not a commercial bank that funds itself with deposits (i.e., checking accounts held by individuals and companies). Instead, it funded itself in the market for overnight loans. This worked perfectly fine for decades, until, as William Cohan wrote in House of Cards, “the funding evaporated like rain in the Sahara.” Much of Wall Street, in other words, was always just 24 hours away from a funding crisis.”

Looking Ahead

· Public Debt: Berkeley’s Barry Eichengreen joined the New Books Network podcast to discuss his work “In Defense of Public Debt.” He recounted how the U.S., France and Britain all brought down their government debts in the decades after major wars—the Civil War in the U.S., for example, and the Napoleonic Wars for Britain. The latter in fact mostly ran primary budget surpluses for almost a century leading up to World War I (the term primary surplus excludes debt payments). Eichengreen warns that this sort of budget discipline is much less likely in today’s world. For one, 19th century voters were typically wealthier, white males that owned bonds—in other words, they were creditors with a financial interest in avoiding inflation. Today’s democracies are much more inclusive. After World War II, meanwhile, governments shrank their debts thanks to rapidly growing economies and populations—the third quarter of the 20th century, Eichengreen said, was “the period of fastest economic growth in the history of the world.” While it’s possible some new and revolutionary, productivity-lifting technologies save the day, demography in most parts of the world foretell a future of slower growth. The professor concludes: “Public debt is a powerful and valuable instrument to deploy in emergencies, be those wars, pandemics, financial crises or whatever. We have just passed through a period marked by successive crises, so we’ve utilized that weapon and kind of depleted our reserves… So I do think it’s imperative now for governments to restore strength in their capacity to borrow, especially given that that capacity will be strained going forward by those higher interest rates. The ways that governments restored that capacity in the past are not going to be available to the same extent today because growth rates are going to be slower than in the mid-20th century [and] budgets surpluses are going to be harder to sustain than in the mid-19th century.” He does end with a bit of hopefulness, suggesting perhaps the green energy and digital revolutions could help boost economic growth. Pure luck is a factor too, as Britain enjoyed during a century of relatively few major military conflicts leading up to World War I.

· The Next Crisis: When the mortgage market triggered a financial collapse in 2008, the Federal Reserve stepped in with various measures of support, including a reduction of overnight interest rates to zero and heavy bond-buying to boost financial sector liquidity. When the Covid epidemic caused another market crisis in early 2020, the Fed again responded by lowering rates to zero and buying bonds. Congress, in both cases, added fiscal support to the Fed’s monetary actions. Alright, so what happens if tomorrow, there’s another major crisis? Would the Fed and Congress respond in a similar fashion? Doing so would be riskier, with federal debt having already grown so much, and with inflation now a significant concern. A crisis would by itself perhaps solve the inflation problem by depressing demand. But the point is, with each successive crisis, the monetary and fiscal stakes get higher. Also keep in mind the links between monetary and fiscal policies—as the Fed raises rates, it becomes more expensive for Congress to borrow, and vice versa.