Econ Weekly (July 12, 2021)

Featured Place: Santa Fe, New Mexico

Inside this Issue:

Mystery of the Treasury: Why Won’t Bond Yields Rise?

Inflation Anticipation: Coming this Week... June’s CPI reading

Yearnings for Earnings: Also this Week, the Start of Q2 Earnings Season

Earnings from Learnings: A Look at For-Profit Universities

Robin Good? Or Bad? The Raging and Praising about Robinhood.com

Mother Trucker: Knight-Swift has a new daughter company

Wake Up! Coffee Costs Surging

The Evolution of Revolutions: Five Great Waves of Innovation (and maybe a Sixth)

The Malady of Inequality: A Princeton Professor Explains

Train Campaign: Amtrak Wants to Add Tracks

Tied to Tuna: American Samoa’s Fishy Dependency

North Star: A Civil War-era Economic Boom

And This Week’s Featured Place: Santa Fe, New Mexico, Old City Attracts Old People

Quote of the Week

“Physical stores remain an important part of our business to build awareness and connect with consumers in a meaningful way, including driving higher loyalty member enrollment.”

-Levi Strauss CEO Chip Bergh

Market QuickLook

The Latest

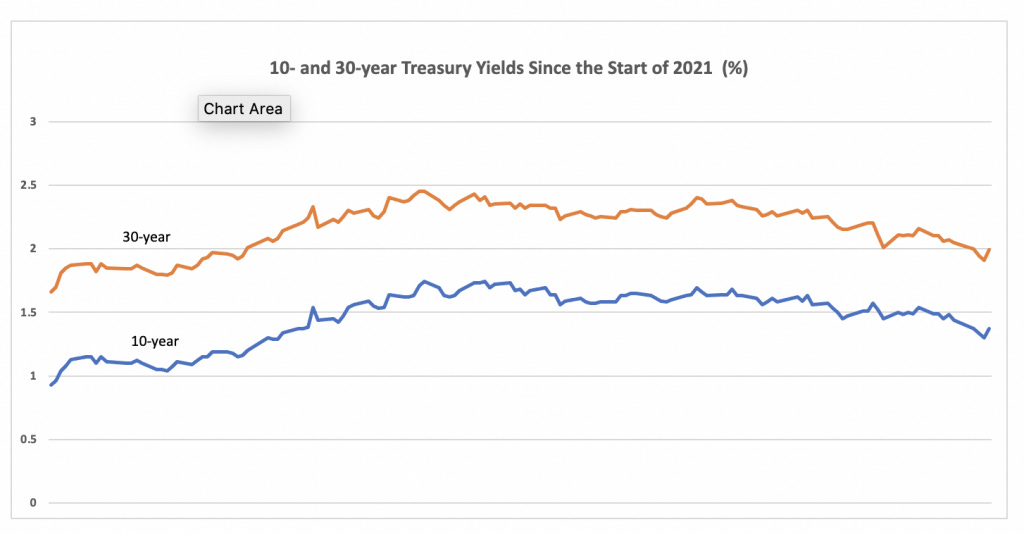

Why won’t interest rates rise? It’s a central question for the economy as the second half of 2021 gets underway.

Yields on newly issued 10-year Treasuries dropped again last week, at one point sharply before a partial recovery. This was not what the market expected earlier in the year, when clear signs of rapid GDP growth and inflation began to drive rates higher. Is the bond market becoming more pessimistic about GDP growth and more skeptical of non-transitory inflation? Perhaps it signals heightened concern about the new Delta variant of the Covid virus. Some are perhaps concerned about the less-than-stellar recovery in labor markets. Perhaps the heightened appetite for safe Treasuries reflects unease about an earlier-than-expected Fed pullback on monetary stimulus—newly-released details of the last FOMC meeting show that talk of tapering has indeed begun. Or maybe, the recent retreat in bond yields merely reflects some near-term technical factors, like idiosyncrasies in the Treasury Department’s cash management.

To be clear, government bond yields should logically increase if GDP and inflation are expected to grow strongly. Or put another way, demand for government bonds should decrease. But it’s not decreasing. And the big question is: Why not?

What does the stock market say? Prices momentarily sank during the week, as those falling bond yields made equity investors think twice about the economy’s prospects. Labor market reports showing 9m unfilled jobs and higher unemployment claims added to the pessimism. But stock prices ultimately recovered, enough to cement yet another weekly gain in major indices.

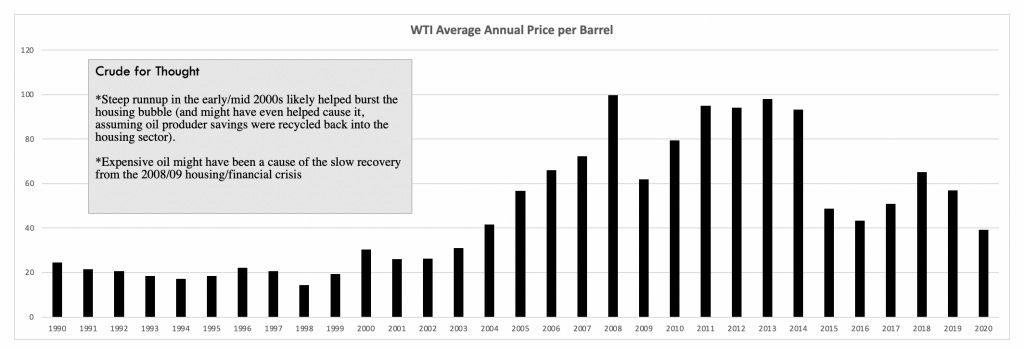

Oil prices, on the other hand, declined last week amid OPEC squabbling. But interestingly, U.S. shale producers—always quick to pump more supply in the past—are behaving more conservatively this time. As a reminder, oil prices are way up from last year’s depressed levels but still—at $75 per barrel—well below their averages in the early 2010s (see chart below). For the U.S., high oil prices are not nearly as harmful as they once were (thanks in part to the 2010s resurgence in U.S. production). But they still induce a significant transfer of wealth from American households to overseas oil producers. They also have the power to curtail the current recovery in leisure travel.

Rising prices, therefore, aren’t a trivial threat to the recovery. Nor are the severe droughts afflicting western states. That’s a threat to agriculture. It’s also a fire hazard. According to the National Interagency Fire Center, federal wildfire suppression costs in the U.S. have spiked from an annual average of about $425m in the 1980s and 1990s, to $1.6b in the last two decades. It’s one manifestation of the perils associated with climate change. And it underscores the epic challenge of transitioning to a carbon-free economy, even while carbon sources of energy remain supremely cost-efficient.

Covid resurgence, a subdued labor recovery, the potential impact of Fed tightening, an oil shock… What else to worry about? Asset bubbles, perhaps? Enormous highly leveraged bets in the crypto market? Hack attacks from abroad? Volatile short-term money markets? U.S.-China tensions? The chronic dysfunctions of the “Three H” markets (see below)? Inflation fears still linger, for sure. And growing in Washington are concerns about concentrated corporate power. Last week, President Biden signed an executive order designed to protect consumers and small businesses from industry giants. Many states, meanwhile, are now suing Google for app store practices no different from those criticized at Apple.

But the American economy—or any economy for the matter—has never been free of worries, threats, risks and fears. Hopefully, Corporate America will ease anxieties as firms start presenting their Q2 earnings reports this week. Tuesday is opening day, with JP Morgan and Goldman Sachs taking center stage. Outside the banking sector, others to watch this week include United Health, PepsiCo and the railroad Kansas City Southern, currently in the process of selling itself to Canadian National. Also reporting in faraway Asia, meanwhile, will be Taiwan Semiconductor (TSMC), a kingpin in its strategically vital industry. Most importantly, earnings season will unveil whether corporate profits are consistent with rising stock prices, and whether corporate sales show any indications of weaker consumer spending. It’s ravenous consumer spending, after all, that’s most responsible for the vigorous recovery in GDP.

It’s not just earnings though. There’s something else the market will be watching this week—watching with even greater interest. On Tuesday, the Department of Labor will publish its consumer price index for June. Will it show inflation cooling off? Or will readings once again be far above the norm?

to read the remainder of this issue, visit www.econweekly.biz