June 7, 2021

Like many U.S. companies in the wake of Covid-19, U.S. railroads are experiencing a state of strong demand and constrained supply. On balance, the situation is mostly favorable, with North America’s Big Seven freight railroads all expected to earn solid profits in 2021. Of course, the Big Seven will soon be the Big Six, assuming regulators approve Canadian National’s $30b takeover of Kansas City Southern. Will it get approved? What do competitors think? What’s the industry’s outlook for the remainder of this year and beyond? Key executives shared their thoughts on these and other hot topics at two major virtual investor events held in recent weeks. One was hosted by Wolfe Research analyst Scott Group and the other by his counterpart at Alliance Bernstein Dave Vernon. Here are some highlights:

Demand: One the demand side, companies spoke of strength across many top products, including metals, grain, fertilizer, lumber, and paper. The intermodal business is especially strong. Chemical shipments—which tend to be high margin—have bounced back from weather disruptions in Texas. Demand in general, furthermore, is more consistent across seasons this year. On the other hand, railroads expressed frustration about weak auto shipments due to the semiconductor shortage. CSX said three-quarters of the auto plants it serves have been impacted by supply shortages; one in fact was shut down for 15 weeks. Manufacturing firms more generally have faced issues restarting production after Covid.

What about coal? There’s no escaping the reality: Coal shipments, a staple of rail freight for more than a century, is in secular decline as the U.S. adopts cleaner forms of power including natural gas and renewables. Still, coal accounts for as much as a tenth of revenues for some rail lines. There’s some good news though: The export market for coal is currently stronger than expected, breathing life into the dying category, if just temporarily.

Supply: CSX, for one, says it has plenty of free track capacity and many additional locomotives it can use as needed. Lines report some issues with staffing but not nearly the dire sort afflicting the trucking sector. That said, railroads are not immune to the supply bottlenecks distressing other parts of the economy. As mentioned, the automaker supply chain problems are resulting in fewer cars and car parts for trains to haul. Severe congestion at west coast ports (most importantly Los Angeles and nearby Long Beach) are also affecting freight volumes. So is a stressed drayage network and limited warehouse capacity.

The pre-Covid situation: Note that the period leading up to Covid wasn’t all that rosy for railroad demand. Trade wars and other factors caused what CSX described as an “industrial recession.” Union Pacific, for example, saw revenues drop 8% from 2018 to 2019.

Looking ahead: CSX’s CFO Kevin Boone forecasted strong revenue per user (RPU) growth for the second half of 2021. “What we know,” he said, “is customers are looking for capacity.” Added CEO James Foote: “Trend lines over the past weeks and months appear very positive.” Most (but not all) of the railroads are responding by hiring more workers. Many are scheduling a lot of overtime which of course inflates costs.

Revenue growth? The industry, make no mistake, has struggled to expand over the past decade. Whereas in some industries, profits are a biproduct of economies of scale induced through growth, railroad profits are more the biproduct of industry consolidation. CSX chief James Foote recalled the early 1980s, when there were still more than 60 Class-1 railroads. One area of the business that is growing at a healthy pace today: Intermodal transport. Norfolk Southern says its intermodal business is growing at a 6% to 7% annual clip. It’s also what the company describes as the “best product railways offer.” For railroads, though, intermodal shipments tend to generate lower revenues per unit.

E-commerce: One source of potential growth is convincing e-commerce players like Amazon to locate warehouses on rail networks, thereby making rail a key part of their supply chains. Historically, shippers tended to avoid railroads if their goods were highly time sensitive. The railroads more generally want to leverage the real estate they own to encourage more industrial development along their rails. They also want to make sure they become an important part of the supply chain for electric vehicle production.

Competition with trucks: The railroads compete with each other, for sure. But they also compete with trucks. Well, right now, the railroads claim to be winning significant market share from their trucking rivals, in part because of the severe trucker labor shortage. And many seem to believe that shortage isn’t going away any time soon. Truck capacity more generally is tight. And the railroaders have another ace up their sleeve: Their ability to pitch a more environmentally friendly service than the trucking sector, with fewer carbon emissions. Eventually, truckers will look to adopt clean electric vehicles or perhaps even hydrogen vehicles. But freight trains too, are looking to go cleaner with renewable diesel power. Note also that as truckers look to autonomous driving, railroads too would like to go driverless.

Service: Most railroads will admit to less than stellar customer service over the years. “Customers haven’t trusted us with our freight historically,” said Boone of CSX. All are making efforts to change that, striving to be more than just transport companies but also solutions providers. Union Pacific CFO Jennifer Hamann spoke of transforming the company’s sales culture. Everyone speaks of improving information technology to improve reliability and service. Note that about half of all rail freight business for some lines involves interchanges with another railroad. So service improvements will in part depend on the whole industry’s efforts.

Covid disruptions: In general, dwell and velocity trends were correlated to Covid cases: When cases rose, speeds declined and dwell time increased.

Pricing: Can the railroads raise prices to offset their rising costs? It’s not so easy, because of longterm contracts with customers. Union Pacific says 30% of its business, including its intermodal business, involves one-year contracts. Norfolk Southern says the average duration of its contracts is more than two years. That said, as contracts come up for renewal, management teams are raising prices where they can.

Consolidation: We’ll get to the big CN-KCS merger in a moment. But CSX is more quietly buying the trucking firm Quality, hoping to improve its wherewithal to ship chemicals, a major product category for CSX. One synergy it hopes to achieve: Coordinating rail-truck movements so that Quality’s drivers won’t have to do as many overnight trips. It’s these overnight trips, keep in mind, that are a leading reason for the trucking industry’s extremely high driver turnover. Just last fall, CSX agreed to buy Pan Am, a regional railroad covering New England. Takeovers aren’t for everyone though—other lines say they’d prefer to just partner with trucking companies.

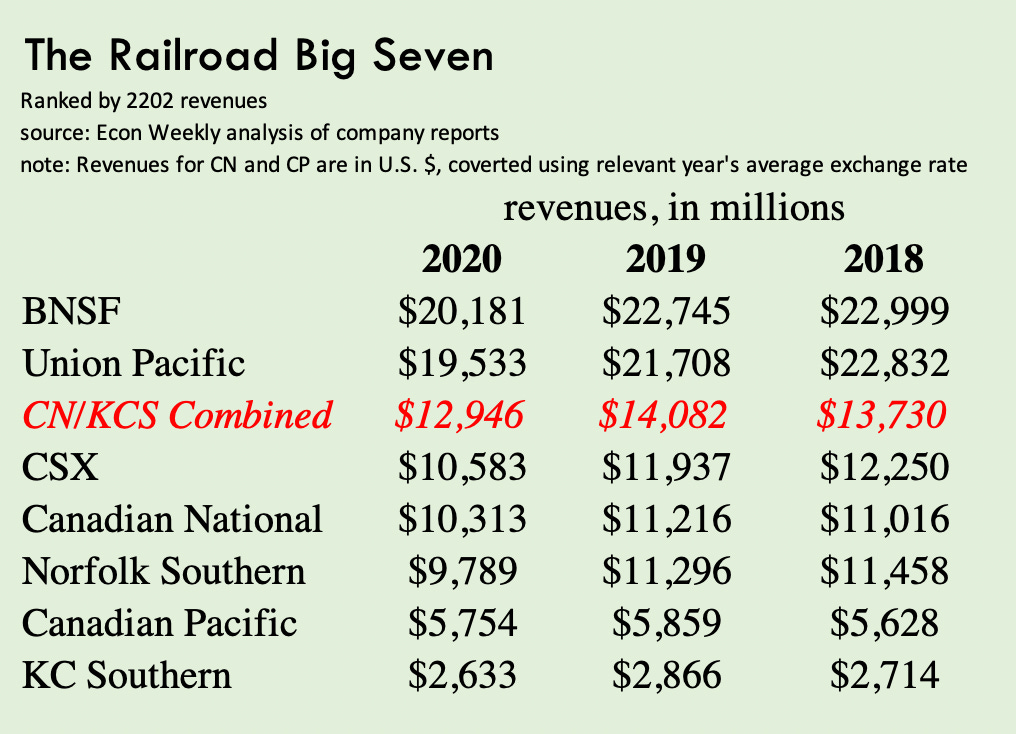

The BIG merger: The chief executives of both Canadian National and Kansas City Southern are now jointly presenting at industry events, with messages for both investors and regulators. CN, remember, outbid rival Canadian Pacific, which made the first offer to buy KCS. Both Canadian companies coveted their U.S. rival’s Mexican network, which accounts for almost half of its total revenues. KCS is also a big player in petroleum and chemical shipments, along with grain and fertilizers. Roughly 13% of its revenues come from intermodal shipments, an area ripe for expansion. For CN, whose core U.S. network runs north-south between Chicago and New Orleans, the KCS acquisition adds a roughly parallel spine from Laredo, Texas, America’s busiest trade gateway, to Kansas City and over to Chicago. This will enable CN to compete for shipments along the extremely busy Interstate-35 corridor, along with the I-55 corridor where it’s already strong. Cross border shipments within North America, meanwhile, are expected to grow as U.S. companies near-shore production from Asia and as an updated U.S.-Mexico-Canada trade agreement takes effect. Currently, the companies said, 42% of all containers arriving in the U.S. are coming from China, but this could change as firms look to reduce their Chinese exposure. CN and KCS insist the $1b in annual operating synergies they’re targeting (over three years) will enable more investment in maintenance, safety, service and information technology. Offering single-line service from Kansas City all the way to the east coast, for example, is a more compelling product for shippers than the interchange offering available today. The combined network also gives Kansas City access to the east coast port of Montreal. Back in Mexico, the companies see the port of Lazaro Cardenas on the country’s Pacific coast as well-placed to take some ocean cargo from the congested twin ports near Los Angeles. KCS, sure enough, has a rail line into the Lazaro port. If that’s not all good enough reason to merge, the two lines say their combined network will be better able to manage through natural disasters and weather events. To further entice regulators to approve, the firms say their merger synergies will enable future job growth. And they’ve pledged to divest their line between New Orleans and Baton Rouge. They hope to close the deal in 2022.

But will it get approved? Rivals want a vigorous review by the U.S. Surface Transportation Board, none more so than Canadian Pacific. Its CEO Keith Creel is adamant that the combination would be uncompetitive and harmful to shippers. Its own proposal, he argues, would be far better for the public and create a much better network. Creel went on to question the value creation its rival is promising. And he sees a newly enlarged Canadian National overly focused on the Illinois Central network it owns to the detriment of investment elsewhere in North America. CN purchased the Illinois Central in 1998, giving it a heavily trafficked line between Chicago and New Orleans.